3 Minutes

If memory chips become the throttle, where does that leave the smartphone race? Qualcomm closed its first fiscal quarter with numbers that beat the street, yet the mood in the boardroom was tempered by a clear caveat: supply, not demand, may dictate growth over the next few months.

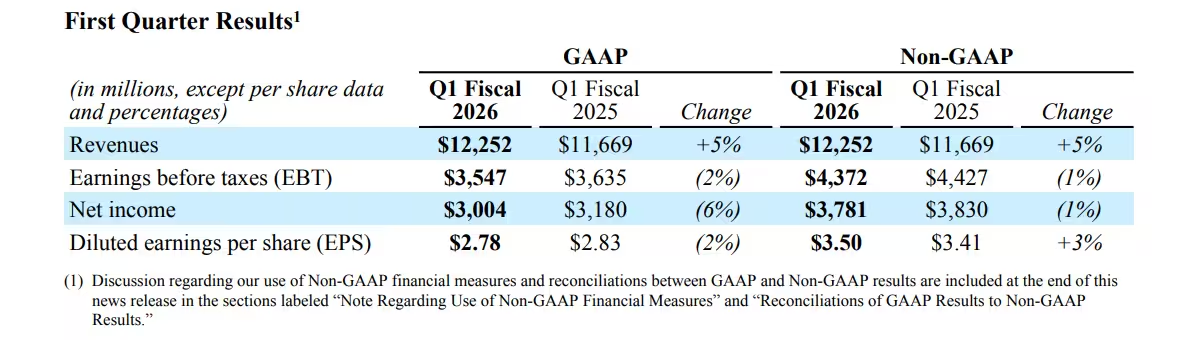

The company reported revenue of $12.25 billion and adjusted EPS of $3.50, edging out analyst estimates of $12.21 billion and $3.41, respectively. Net income came in at $3.0 billion, or $2.78 per share, compared with $3.18 billion and $2.83 per share a year earlier. Small beats. Not a blowout. Still, solid.

Smartphone chips remained Qualcomm's largest engine, bringing in $7.82 billion — up about 3% from the prior quarter. Licensing revenue, driven largely by 5G patents and other IP, added $1.59 billion. The Internet of Things unit, which supplies low-power silicon for industrial devices and consumer wearables, including AR hardware, grew 9% to $1.69 billion. Automotive revenue climbed fastest, up 15% to reach roughly $1.1 billion.

And yet the company offered cautious guidance for Q2: revenue of $10.2 billion to $11 billion and adjusted EPS between $2.45 and $2.65. Analysts had penciled in about $11.11 billion and $2.89. The shortfall ties back to memory availability — not a problem Qualcomm faces directly, but one that affects its customers who buy the memory that goes into phones and other devices.

Memory supply — not consumer demand — looks set to cap mobile growth this quarter.

Why does memory matter so much? Because component shortages change the math for handset makers. If DRAM and NAND become pricier or scarcer, manufacturers face hard choices: absorb costs, lift prices, or slow production. Flagship phones carry higher margins and can better weather component swings. That works in Qualcomm's favor; CEO Cristiano Amon has repeatedly said the company is most competitive in the premium segment.

Investors also got a reminder that Qualcomm returns cash to shareholders. In Q1 the company bought back 15 million shares for about $2.6 billion and paid $949 million in dividends, or $0.89 per share. That kind of capital allocation keeps a steady floor under the stock even when guidance slips.

So what should readers watch next? Keep an eye on memory pricing and OEM purchasing patterns. If component costs normalize, handset makers could accelerate build plans and Qualcomm's next guidance could rebound. If not, the industry may see a shift toward higher-margin devices while mid-tier volumes get squeezed.

Markets change on tiny bottlenecks. This one looks like a memory chip problem that could redraw near-term winners and losers in mobile.

Source: gsmarena

Leave a Comment