3 Minutes

Apple has opened 2026 the way it ended last year: on top. The iPhone maker has kept its grip on the global smartphone market, even as the wider industry wrestles with slower demand, tighter margins, and a stubbornly expensive component supply chain.

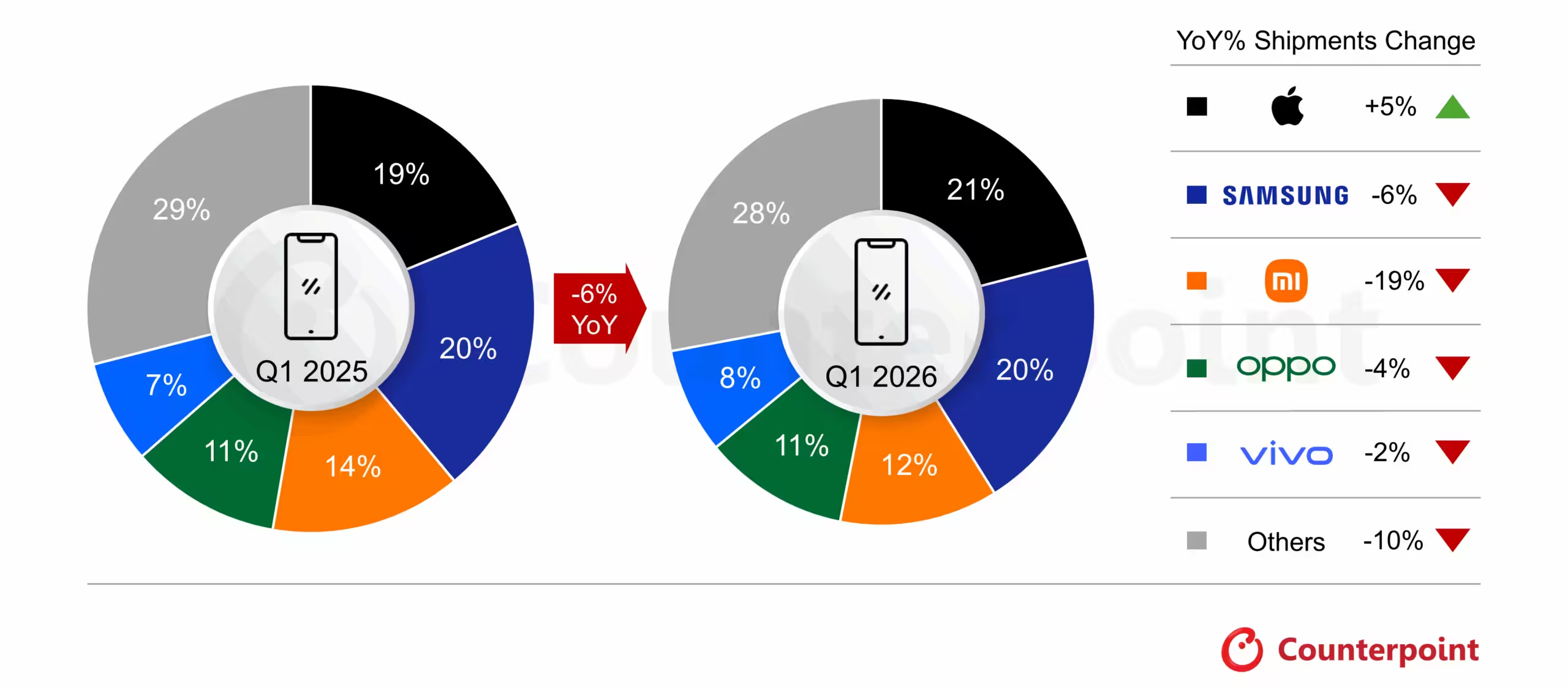

What is helping Apple stay ahead is no mystery. The iPhone 17 lineup continues to sell strongly, while trade-in offers and deep ecosystem loyalty keep buyers inside the company’s orbit. In a market where switching phones can feel like switching entire digital lives, that matters.

Samsung, meanwhile, is still breathing down Apple’s neck. The Korean giant sits just one point behind with a 20% share, but the story is more complicated than the ranking suggests. Shipments fell 6% year over year, with analysts pointing to the later-than-expected Galaxy S26 launch and weaker momentum in the entry-level segment. Even so, early sales data for the new model has been strong enough to hint at a possible rebound later in the second quarter.

Xiaomi remains in third place with 12% of the market, though the pressure is mounting. The company posted a sharp 19% annual decline, reflecting how badly the ongoing memory and semiconductor crunch is hitting brands that depend heavily on affordable devices. When component prices rise, low-cost makers feel it first and hardest. There is less room to absorb the blow.

OPPO, including realme and OnePlus, holds 11% of the global market, while Vivo sits at 8%. Both are facing the same uncomfortable backdrop: softer consumer spending, rising costs, and a market that no longer rewards volume alone. The old playbook is getting thinner by the month.

Profit is replacing pure scale

Counterpoint Research’s latest numbers point to a broader shift across the industry. OEMs are no longer chasing shipment growth at any cost. Instead, they are trimming product lines, cutting weaker models, and leaning harder into efficiency. Refurbished smartphones are also becoming more important, especially for price-conscious buyers who still want a recognizable brand without paying flagship prices.

That pivot makes sense. With memory prices still elevated, manufacturers are being forced to rethink everything from launch timing to hardware configurations. The next phase of 2026 is likely to be less about flooding the market with devices and more about protecting margins in a market where every component counts.

For now, Apple remains the leader. Samsung is close enough to make things interesting. And the rest of the industry is being pushed into a quieter, more disciplined race where survival may depend less on scale and more on strategy.

Leave a Comment