3 Minutes

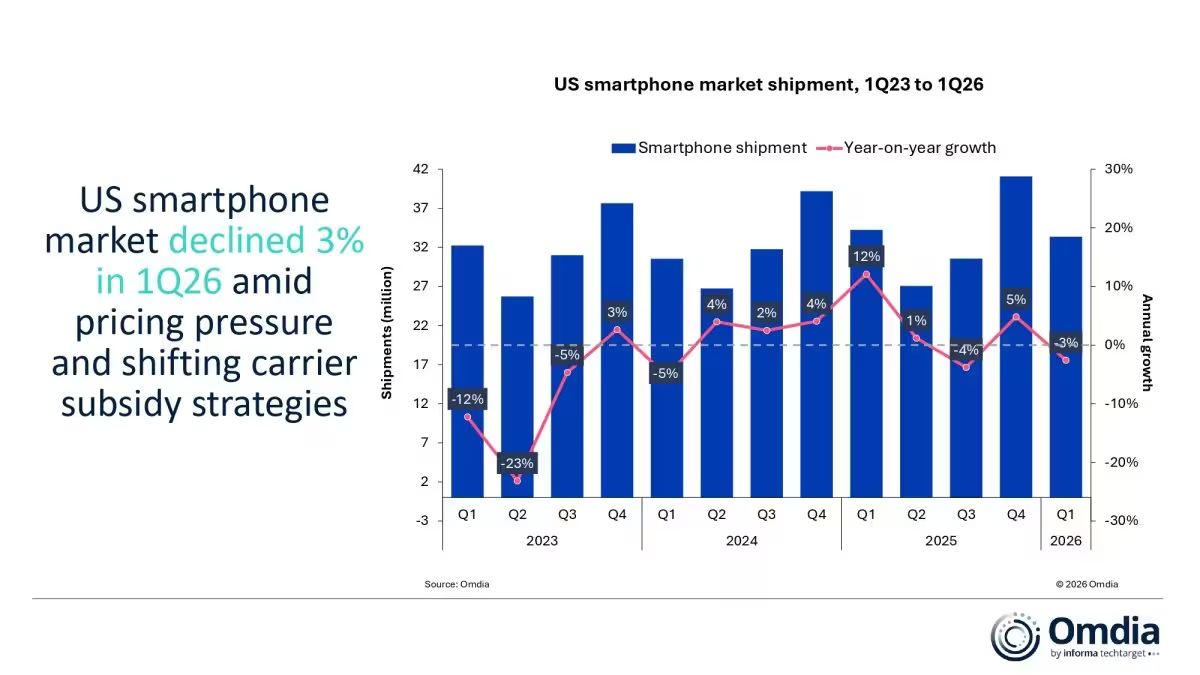

Sales stumbled out of the gate in 2026. The US smartphone market contracted by 3 percent year over year in the first quarter, slipping to 33.4 million units, according to Omdia. It is a small move on the surface, but the forces behind it hint at something messier than a seasonal wobble.

Manufacturers started the year carrying baggage. In Q1 2025 many brands stockpiled inventory ahead of import tariffs introduced by the Trump Administration, and that artificial front-loading left a weaker demand tail in Q1 2026. Add rising memory chip costs and a general consumer pause on upgrades, and you get a market that feels squeezed from both supply and demand sides.

Shifts inside the rankings and the premium tug-of-war

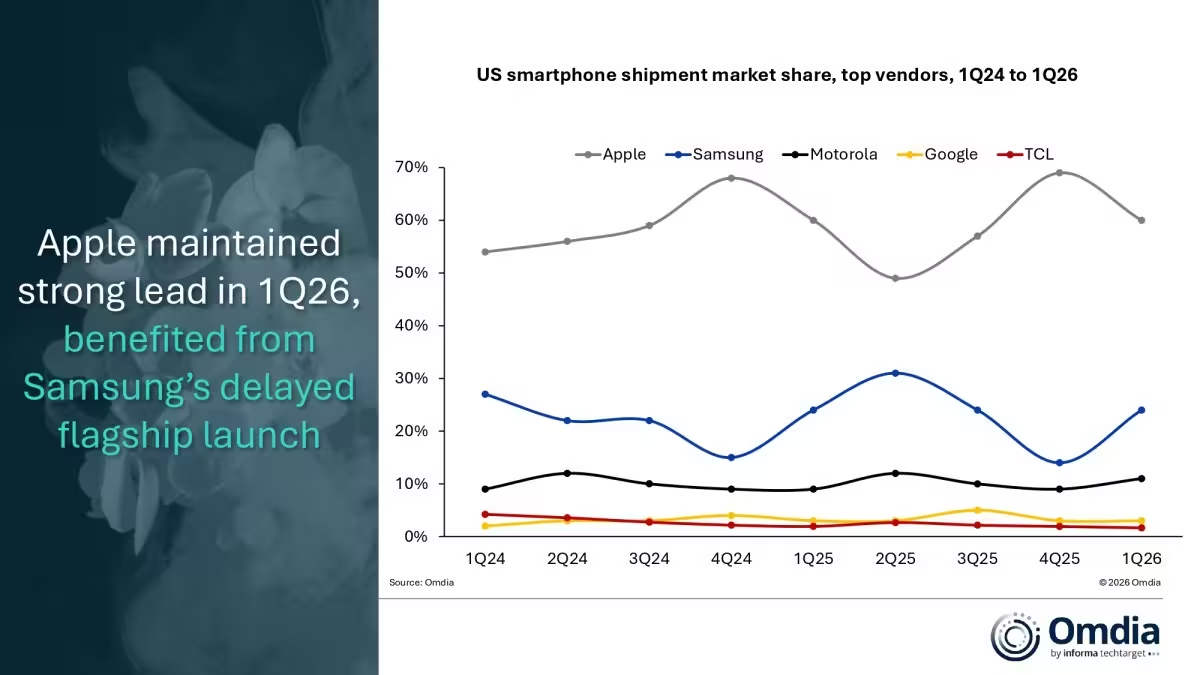

Apple remained the market leader, but shipments fell by 3 percent. The iPhone 17 dominated the company’s tally, making up 70 percent of Apple’s shipments as many buyers chose the new model instead of waiting. Samsung kept the second position, yet its volumes declined by 5 percent. The Galaxy S26 arrived roughly a month later than last year, compressing sell-through. Still, the S26 generated about 25 percent more pre-orders than the S25 did.

Motorola was the standout. It grew shipments by 18 percent thanks to an updated Moto G line that accounted for more than 70 percent of its volume. Google slipped by 7 percent as Pixel 10 sales stagnated and an early Pixel 10a release could not fully revive momentum.

What emerges is a market quietly polarizing. The lowest-price tier proved surprisingly resilient: the under-€276 segment grew by 8 percent. At the other end, premium phones priced above €736 declined only 1 percent. The mid-range took the hit. Devices priced between €276 and €551 dropped 19 percent, while the €552 to €644 bracket fell 6 percent. Consumers are either trading down to cheaper handsets or still willing to spend on top-tier phones, leaving the middle squeezed.

So where does the industry go from here? Analysts point to carrier partnerships as the pressure valve. Plan-linked promotions and closer collaboration with US carriers can blunt the pass-through of rising component costs and keep devices moving. It is not a silver bullet, but it is a pragmatic lever.

Omdia’s outlook is cautious. After the Q1 decline and the current cost environment, they expect the full US smartphone market to shrink around 4 percent in 2026. Small percentage points, yes, but enough to force strategy shifts: launch timing matters, inventory planning matters more, and mid-range portfolios may need reinvention.

Pick a line of sight and the picture is consistent: a market rebalancing under cost pressure and changing consumer priorities. Brands that read that change faster, and work closer with carriers and promotions, will have the best chance of steadying sales in the months ahead.

Source: gsmarena

Comments

Reza

I've seen this in retail ops, inventory timing kills midrange lines. Carriers help but promos cant fix bad planning. Quick fix? nope, overhaul needed.

mechbyte

Is this even true? Tariff front-loading sounds plausible, but a 3% dip feels smallish... midrange collapsing tho, that's odd. who’s buying cheap?

Leave a Comment