11 Minutes

If you walk into any co-working space in Shoreditch, Kreuzberg, or Naujamiestis today, you can feel a distinct shift in the air. For fifteen years, the silence of these rooms was broken only by the furious typing of code. The dream was digital. The goal was to build a platform, a marketplace, a SaaS tool that lived in the cloud, scaled infinitely, and required zero physical interaction with the real world.

The logic was flawless: Bits are cheap to move. Atoms are expensive. Why deal with shipping containers, customs, and factory defects when you can just push an update to AWS?

But as the sun sets on 2025, that logic has collapsed. The "App Store Era"—the golden age of pure software—is effectively over.

We are entering 2026, a year that will be defined not by who can write the best code, but by who can build the best machine. We are witnessing the Revenge of Atoms.

In this extensive report, Smarti Live dissects why the smart money in Europe has abruptly pivoted from SaaS to DeepTech, why "Hardware is Hard" is now a feature rather than a bug, and why the industrial heritage of the Baltics and Central Eastern Europe (CEE) has positioned this region to win the next decade.

Part I: The Great Commoditization of Code

To understand why hardware is back, we must first understand why software lost its crown.

For a decade, Venture Capitalists (VCs) operated on a simple heuristic: Software has 90% gross margins. Hardware has 30% gross margins. Therefore, invest in software. This created a glut of capital chasing increasingly marginal digital problems. We didn't solve climate change; we solved "15-minute grocery delivery." We didn't fix the energy grid; we built another B2B project management tool.

The AI Deflationary Event

Then came Generative AI. By 2024 and 2025, AI models like GPT-5 and Gemini Ultra had become proficient enough to write production-level code. This was a deflationary event for software.

Lower Barrier to Entry: In 2015, building a complex SaaS platform required a team of 20 engineers and $2 million. In 2026, a single founder with an AI co-pilot can build the same platform in a month for $5,000.

The Moat Evaporation: In business, a "moat" is your defense against competitors. If your code is your only moat, and AI allows anyone to replicate your code instantly, you have no moat.

We are now seeing a tsunami of "Wrapper Startups"—companies that are just thin interfaces over AI models—being wiped out. The market is flooded with software. When supply becomes infinite, price approaches zero. The days of getting a 100x valuation multiplier for a simple SaaS app are gone.

Part II: Why "Hardware is Hard" is the New Gold

For years, VCs used the phrase "Hardware is Hard" as a dismissal. It meant: "Don't show me your pitch deck." It implied capital intensity, supply chain risks, and slow iteration cycles.

In 2026, the narrative has flipped. Hardware is Hard, and that is exactly why it is valuable.

In a world where digital products can be cloned in seconds, physical complexity is the ultimate defensive moat. You cannot ask ChatGPT to 3D print a proprietary photonic laser chip. You cannot ask an LLM to manufacture a long-range autonomous drone with anti-jamming capabilities. You cannot prompt-engineer a bio-reactor that turns algae into fuel.

These things require physics. They require factories. They require supply chains. And because they are hard to build, they are impossible to copy quickly.

The Return of "Capex" (Capital Expenditure)

Investors have realized that the companies with the most enduring value are those that touch the physical world. Look at the biggest success stories of late 2025 in Europe:

Northvolt (Sweden/Germany): Batteries.

Isar Aerospace (Germany): Rockets.

Skeleton Technologies (Estonia): Supercapacitors.

Brolis (Lithuania): Semiconductors/Defense.

None of these are "Apps." They are industrial giants in the making. They require massive upfront capital (Capex), but once they are operational, they own the market for decades.

Part III: The Geopolitical Catalyst – "Strategic Autonomy"

We cannot talk about the shift to hardware without talking about the war and the geopolitical fragmentation of the world.

The globalization era of "Design in California, Manufacture in Shenzhen" is dead. The supply chain shocks of the early 2020s and the rising tensions between major powers have forced Europe to wake up. The buzzword in Brussels and Berlin is "Strategic Autonomy."

Europe has realized it cannot rely on Asia for its chips, batteries, and medicine, nor can it rely entirely on the US for its defense.

The DefenseTech Boom

This is the elephant in the room. For decades, European VCs were forbidden by their Limited Partners (LPs) from investing in anything related to "military" or "defense." In 2026, that taboo has been shattered. The war in Ukraine taught the Baltic region a harsh lesson: Software doesn't stop tanks. Hardware stops tanks.

This has birthed a massive ecosystem of "Dual-Use" technology startups in Lithuania, Poland, and Estonia.

Drones & Robotics: Startups building autonomous systems that can monitor borders or deliver medical supplies (civilian) but also perform reconnaissance (military).

Cyber-Physical Systems: Protecting power grids and water plants from physical and digital attacks.

The NATO Innovation Fund and initiatives like DIANA (Defence Innovation Accelerator for the North Atlantic) are pumping billions into hardware startups in this region. This is "Patient Capital"—money that doesn't need a return in 3 years, but expects strategic dominance in 10.

Part IV: The Baltic Advantage – Why We Win at Atoms

This global pivot to DeepTech and Hardware plays perfectly into the hands of the Baltic and Central Eastern European (CEE) ecosystem. To put it bluntly: We were never that good at consumer marketing, but we are excellent engineers.

While London and Paris excelled at building "Brands" and B2C marketplaces, the CEE region kept its head down and focused on STEM (Science, Technology, Engineering, Mathematics).

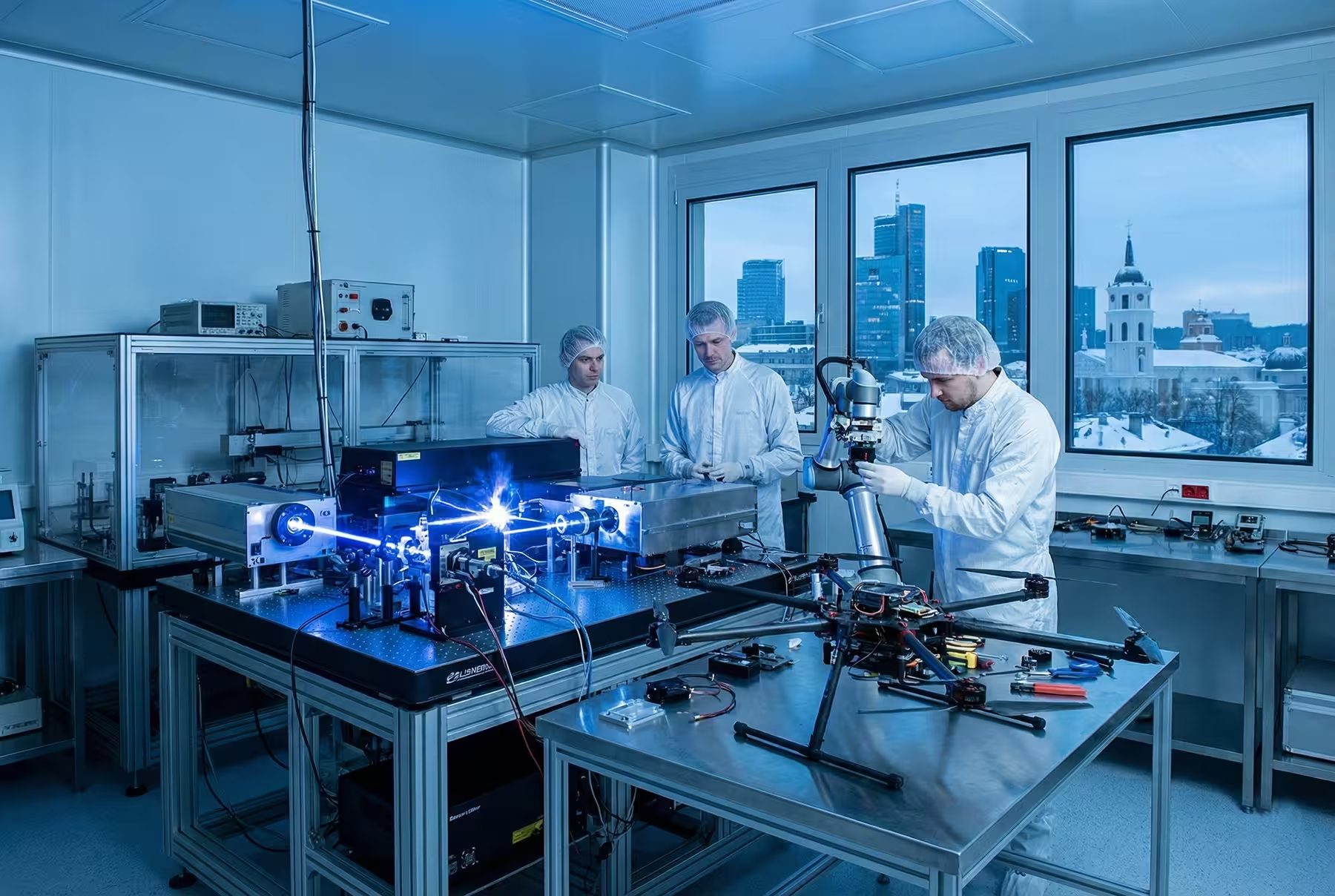

1. The Laser Legacy of Lithuania

Take Lithuania as a prime example. It is not famous for social networks. It is famous for Lasers. Lithuania holds a staggering share of the global scientific laser market. This wasn't an accident; it was a 50-year investment in physics. Now, as the world demands high-precision manufacturing, semiconductors, and fusion energy research (all of which need lasers), Lithuania is sitting on a goldmine. Startups here aren't trying to build the next Instagram. They are building the machines that build the chips that run Instagram.

2. The Manufacturing Hub of Poland & Czechia

Poland has effectively become the factory of Europe. But in 2026, it is no longer about cheap labor; it is about "Smart Manufacturing" (Industry 4.0). Startups in Warsaw and Prague are building the robotics and IoT layers that automate these factories. They are merging the region's software prowess with its industrial base.

3. The Estonian Robotics Sandbox

Estonia, famous for its digital governance, has quietly become the world's testing ground for autonomous robots. Walk around Tallinn in 2025, and you dodge more delivery robots than pigeons. This regulatory openness has attracted hardware founders from all over the world to test their "Atoms" in a real-world environment.

Part V: The New Playbook for Founders

If you are a founder reading this in 2026, the advice "move fast and break things" needs an update. When you are dealing with atoms, if you break things, people get hurt or factories shut down.

The new playbook for the Hardware/DeepTech founder involves:

1. The "First Customer" Strategy

In SaaS, you build a Beta and look for users. In DeepTech, you find a customer (often a government or a large industrial corp) before you build. You need "Off-take Agreements"—contracts that say, "If you build this robot/chip/battery, we will buy it." This validates the market and allows you to raise debt financing for your factory, preserving your equity.

2. Bridging the Valley of Death

Hardware startups face the "Valley of Death" between the prototype phase and mass production. Smart founders in 2026 are using "Hybrid Funding":

Venture Capital: For R&D and team growth.

Grants (EU/National): For high-risk research (non-dilutive).

Venture Debt: For buying equipment and inventory.

3. Vertical AI

This is where software still matters. The most successful hardware companies of 2026 are heavily AI-enabled. They don't sell "a camera." They sell "an AI-powered perception system." The hardware is the body; the AI is the brain. But—and this is critical—the value is captured by the body. You can copy the AI model, but you cannot copy the proprietary sensor data that the hardware collects.

Part VI: The Investor's Perspective – "Boring is Sexy"

We spoke to a Partner at a leading Baltic VC fund (who requested anonymity) about their 2026 thesis. Their answer was revealing:

"Three years ago, I wanted to see growth metrics, churn rates, and virality. Today, I want to see patents. I want to see a factory floor plan. I want to see something that I can kick. If a startup tells me they are building a 'platform', I fall asleep. If they tell me they are building a new propulsion system for maritime logistics, I'm listening. Boring is the new sexy."

This shift is driven by the realization that Real Problems bring Real Returns. Selling ads on a social network is a fake problem. Storing renewable energy is a real problem. Securing a nation's borders is a real problem. Feeding a growing population with synthetic biology is a real problem.

DeepTech companies take longer to mature (7-10 years vs. 5-7 years for SaaS), but their exit outcomes are binary: either they fail, or they become essential infrastructure for the global economy.

Part VII: Conclusion – The Industrial Renaissance

The pendulum of history swings back and forth. We spent the last 20 years in the clouds, digitized and abstracted. Now, gravity is pulling us back to earth.

The "App Store Era" was a time of convenience and entertainment. It gave us great tools, but it didn't fundamentally change the physical reality of our planet. The next era—the era of 2026 and beyond—will be defined by the mastery of matter.

For the Baltic and CEE region, this is not a threat; it is a homecoming. We are returning to what we have always been best at: Hard engineering, resilience, and building things that last.

So, to the founders sitting in those co-working spaces: Close your IDE. Open CAD. Go visit a factory. The world doesn't need another app. It needs a better machine.

Welcome to the world of Atoms.

Comments

Tomas

Nice rallying cry but feels a bit romanticized. Not every region can pivot to heavy industry overnight, and env impacts?

labcore

I've seen this in my lab, lasers and sensors are where the IP lives. Not flashy but oof, takes forever to commercialize, grants saved us tho

turbo_mk

Hardware is hard they said... but is Europe really ready to scale mass production? Who's funding 10+ years? feels fuzzy, imo

mechbyte

wow didn't expect that shift, kinda thrilling and scary. factories over apps? If capex wins, who loses? curious about timelines, and jobs.

Leave a Comment